COMPANY OVERVIEW

The company was incorporated on December 23, 2014 and began operations on August 23, 2015 when Bandhan Financial Services Limited (“BFSL”), their ultimate parent company, transferred its entire micro-finance business to them and they simultaneously commenced general banking activities. Bandhan Konnagar was formed in 2001 as a non-governmental organisation (“NGO”) providing micro-finance services to socially and economically disadvantaged women in rural West Bengal. BFSL started its micro-finance business in 2006 and the NGO transferred its micro-finance business to BFSL in 2009 and thereby the entire micro-finance business was undertaken by BFSL. By the time BFSL transferred its micro-finance business to Bandhan Bank ltd., it was India’s largest micro-finance company by number of customers and size of loan portfolio. They believe that the “Bandhan” brand is instrumental to their success.

The company was incorporated on December 23, 2014 and began operations on August 23, 2015 when Bandhan Financial Services Limited (“BFSL”), their ultimate parent company, transferred its entire micro-finance business to them and they simultaneously commenced general banking activities. Bandhan Konnagar was formed in 2001 as a non-governmental organisation (“NGO”) providing micro-finance services to socially and economically disadvantaged women in rural West Bengal. BFSL started its micro-finance business in 2006 and the NGO transferred its micro-finance business to BFSL in 2009 and thereby the entire micro-finance business was undertaken by BFSL. By the time BFSL transferred its micro-finance business to Bandhan Bank ltd., it was India’s largest micro-finance company by number of customers and size of loan portfolio. They believe that the “Bandhan” brand is instrumental to their success.

Bandhan Bank Limited is Kolkata, West Bengal based commercial bank focused on micro banking and general banking services. Bandhan Bank has a license to provide banking services pan-India across customer segments. Bank offer a variety of asset and liability products and services designed for micro banking and general banking, as well as other banking products and services to generate non-interest income.

The bank has network of 2,546 doorstep service centres (DSCs) and 9.47 million micro loan customers, the bank has strong very hold in microfinance. Bandhan bank has 864 bank branches and 386 ATMs serving over 1.87 million general banking customers. Banks distribution network is strong in East and Northeast India, with West Bengal, Assam and Bihar.

Variety of Products:

-

Retail loans including micro loans, SME loans and small enterprise loans

-

Savings accounts, current accounts and a variety of fixed deposit accounts

-

Other banking products and services including debit cards, internet banking, mobile banking, EDC-POS terminals, online bill payment services and the distribution of third-party general insurance products and mutual fund products.

ISSUE DETAILS

- Issue Open : 15th March, 2018

- Issue Closes : 19th March, 2018

- Issue Type : Book Built Issue IPO

- Face Value : Rs10/ Equity Shares

- Issue Price : Rs.370– Rs.375/ Equity Share

- Valuation : Rs 4470 Cr.(Approx.)

- Market Lot : 40 Shares

- Minimum Order Quantity: 40 Shares and in multiples

- Listing At : BSE, NSE

TENTATIVE DATES

-

Basis of Allotment(Finalization) : 22nd March, 2018

- Refund Initiation : 23rd March, 2018

- Crediting of Shares : 26th March, 2018

- Commencement of Trading : 27th Match, 2018

ISSUE OBJECTS

-

The object of the fresh issue is to augment Bank’s Tier-I capital base to meet Bank’s future capital requirements.

-

Selling Shareholders(OFS) will be entitled to the respective portion of the proceeds of the Offer for Sale.

COMPANY PROMOTERS

BFHL, BFSL, FIT and NEFIT

HISTORY OF THE EQUITY SHARE CAPITAL HELD BY PROMOTERS

Except BFHL, none of the copanies Promoter holds any Equity Shares in the Bank. As on the date of Draft Red Herring Prospectus, BFHL holds 981,483,046 Equity Shares, equivalent to 89.62% of the issued, subscribed and paid-up Equity Share capital of the Bank.

Build-up of the shareholding of BFHL in the Bank

The details regarding the shareholding of BFHL since incorporation of our Bank is set forth in the table below.

All the Equity Shares held by BFHL were fully paid-up on the respective dates of allotment of such Equity Shares.

As of the date of this Draft Red Herring Prospectus, none of the Equity Shares held by BFHL are pledged.

COMPETITIVE STRENGTHS OF COMPANY

-

Operating Model Focused on Serving Underbanked and Underpenetrated Markets

-

Consistent Track Record of Growing a Quality Asset and Liability Franchise

-

Extensive, Low Cost Distribution Network

-

Provide accessible, simple, cost-effective and innovative financial solutions

-

Robust Capital Base

-

Maintaining focus on micro lending while expanding further into other retail and SME lending

INDUSTRY OVERVIEW

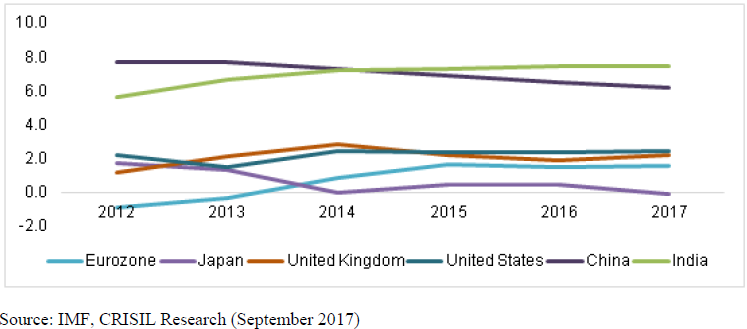

India is one of the fastest-growing economies in the world. Over the past three fiscal years, India has grown as a result of an improved growth-inflation mix. Fiscal and monetary policies have focused on raising both the quality and rate of growth while reducing India’s deficit. The Government of India has adopted a framework targeting inflation while modernising its central banking system. Consequently, CRISIL views an improvement in India’s financial stability and ability to withstand global economic events in comparison with the past.

GDP growth (percentage change)

CRISIL Research estimates GDP growth in fiscal year 2018 at 7% driven by growth in agriculture and services sector while Nomura sees GDP growth @7.5% in the same fiscal year.

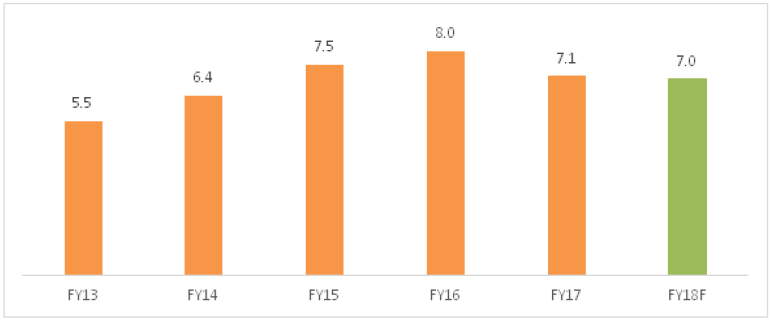

Annual GDP growth (%)

Trend in household savings and financial savings

Trends in savings in financial assets

VALUATIONS

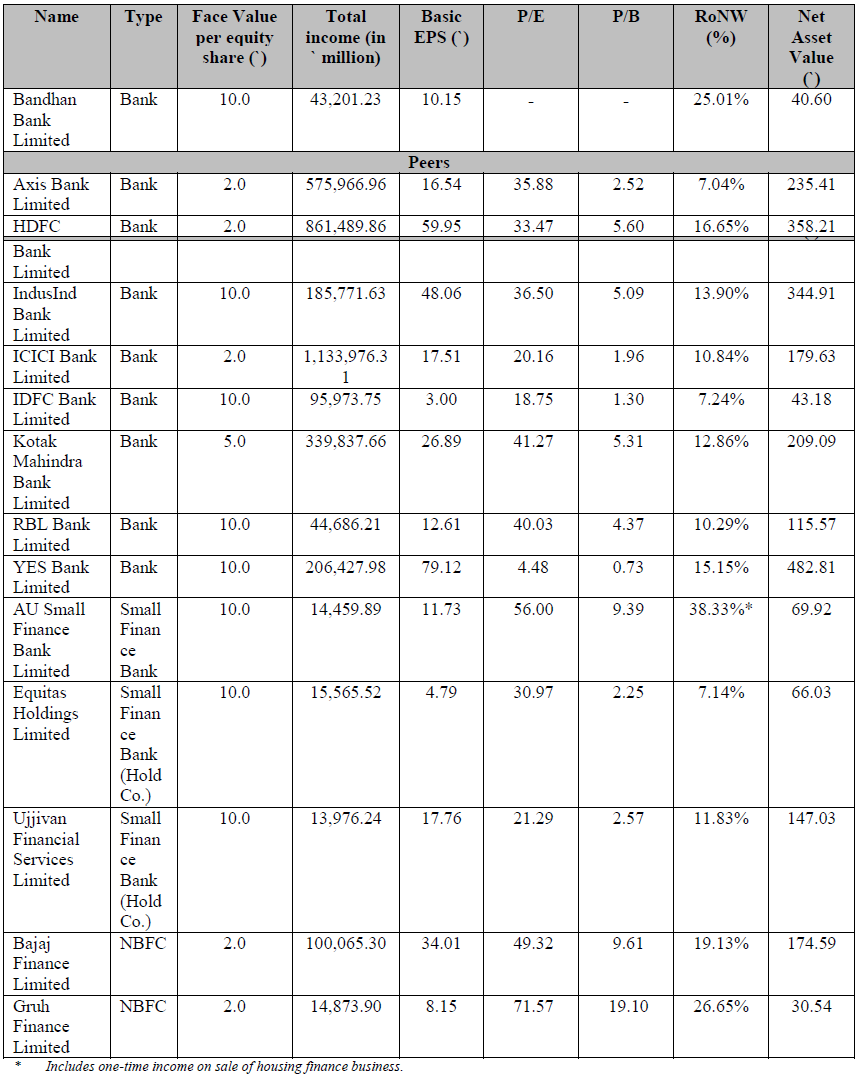

As we talk about the valuations the stock is marginally overvalued with a P/E of 36.95x at the upper price band and 36.45x on lower price band as compared to already listed peers but when it comes to the Industry PE then its @ highly discounted valuation

INDUSTRY PEER GROUP P/E RATIO

EARNINGS PER SHARE

RoNW

NAV (NET ASSET VALUE)

-

Net asset value per Equity Share as on December 31, 2017 is ₹ 49.35.

-

Net asset value per Equity Share as on March 31, 2017 is ₹ 40.60.

COMPARISON WITH LISTED PEERS

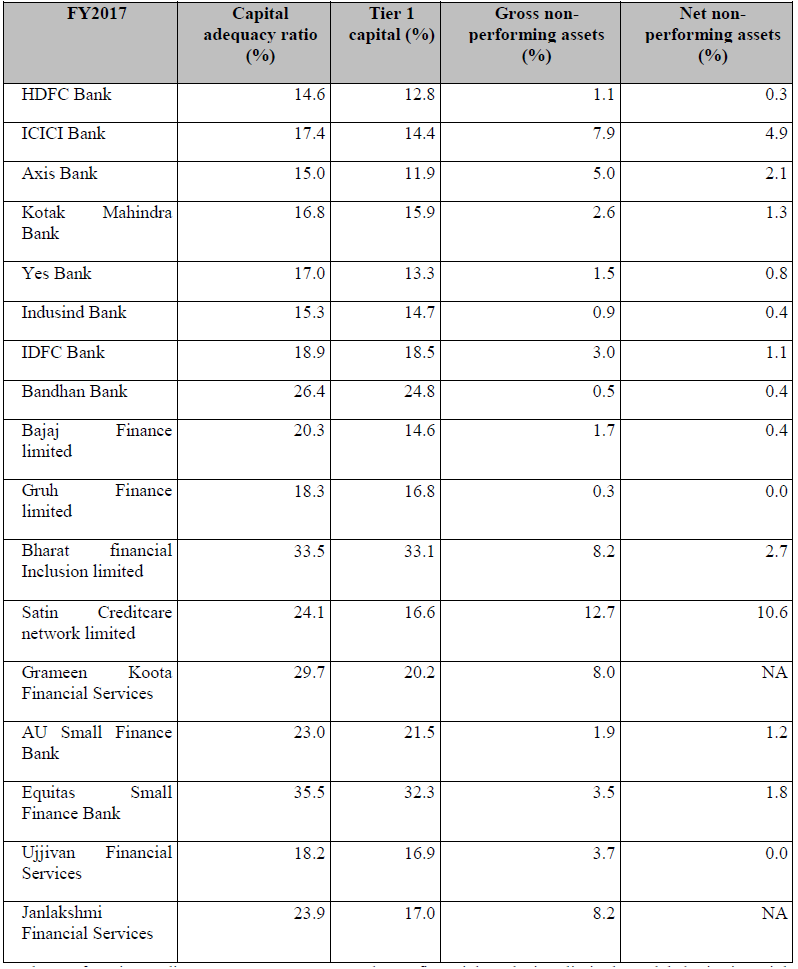

NPA LEVEL LOWEST AMONG PEERS

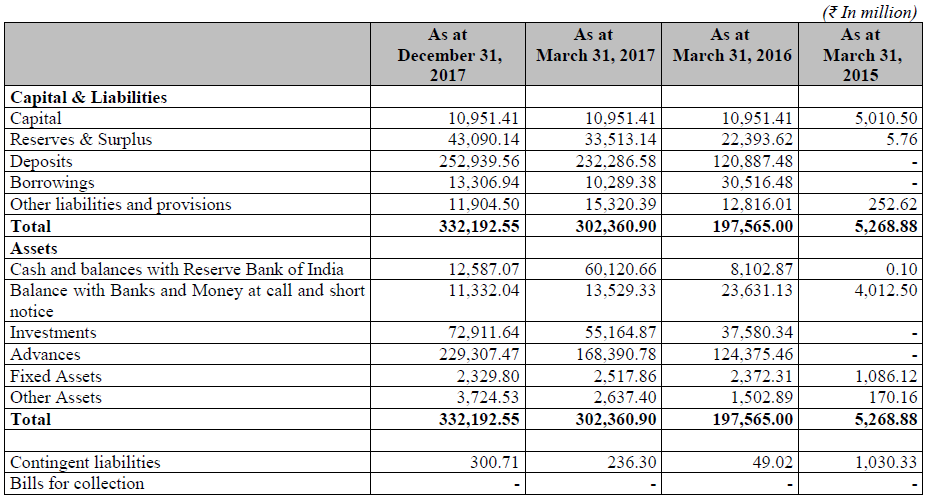

RESTATED FINANCIAL POSITION SUMMARY

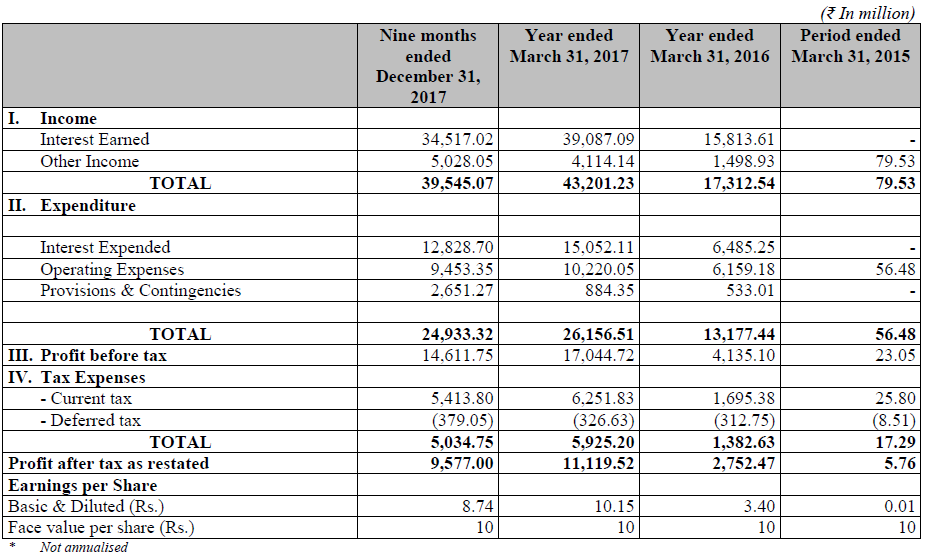

RESTATED STATEMENT OF PROFIT & LOSS ACCOUNT

ANALYSIS & SUBSCRIPTION SUGGESTIONS BY AUTHOR

Fellas what makes this IPO interesting is NPA’s. We have already seen with the PNB scam which has haunted the nation as biggest banking scam in Indian history that these NPA’s leads to bad financial health over the passage of time and we are here on the positive side although its a new bank and its obvious that new bank is not likely to attract that quantum of NPA’s but it shall surely rise with passage of time so does the earnings never the less the bank is said to have the lowest NPA i.e. 0.4% in comparison to its already listed peers in SCB’s.

But we cannot just choose to go for the IPO on NPA factor for coming to conclusion. Let’s have a look on major things to consider before rushing to put money in the company:

-

Valuations: As far as valuations are concerned IPO seems to be marginally over-valued as compared to its already listed peers but when it comes to Industry PE from its highest @71.57 it is highly discounted one ,

-

RoNW/EPS: What a spectacular growth shown although we know its a new bank and these ratios are naturally to be grown over the passage of time but good increment in RoNW and EPS both.

-

Earnings: As seen in other ratios earnings have also shown exponential growth.

-

NPA’s: What this sector has seen lately specially with the PNB scam NPA’s has been the reason for bad financial conditions of the Indian banks which is here our positive point as the the bank is said to have the lowest NPA(0.4%) among its already listed peers.

Fellas a lot of things we have seen positive infact GMP is said to be Rs. 40-50 of the IPO but what has been haunting in the market is pressure on banking sector and its hard for a bank to get subscription when the sector is going on with hard times and Valuations seems to be a bit higher as we have seen better earnings in YES BANK and ICICI BANK having even lower valuations but we have more of the positive things than negative besides these as the bank has just started and there is lot more things coming…. Good things are coming(If it continued to grow @ current rate) we might see some good returns over long term period as its had to say that the issue may fetch higher listing gains due to pressure on banking sector but it shall surely give good returns over medium to long term period .*

*Disclaimer: Author may or may not have interest in the issue, before getting to conclusion consult your Financial Adviser. The Author shall not be responsible for any kind of loss of gain arising out of any investments. All data were taken from RHP filled to SEBI by the company.