COMPANY OVERVIEW

The company is market leader in the RAC OEM/ODM industry in India with a market share of 55.4% in terms of volume in Fiscal 2017 (Source: F&S Report). The company is one-stop solutions provider for the major brands in the RAC industry and currently serve eight out of the 10 top RAC brands in India (Source: F&S Report).

The company is market leader in the RAC OEM/ODM industry in India with a market share of 55.4% in terms of volume in Fiscal 2017 (Source: F&S Report). The company is one-stop solutions provider for the major brands in the RAC industry and currently serve eight out of the 10 top RAC brands in India (Source: F&S Report).

The diversified product portfolio as set out below:

1. Room Air Conditioners (RACs) – This includes window air conditioners and indoor units and outdoor units of split air conditioners.

2. RAC Components – Critical and reliability functional components of RACs such as heat exchangers, motors and multi-flow condensers.

3. Other Components – Other related components including case liners for refrigerator, plastic extrusion sheets for consumer durables and automobile industry, sheet metal components for microwave, washing machine tub assemblies and for automobiles and metal ceiling industries.

Company has a dedicated R&D center located at our Rajpura facility which is equipped with a psychometric lab which is accredited by National Accreditation Board for Testing and Calibration Laboratories (NABL) with ISO/IEC 17025:2005 certification and facilities for 3D modelling, quality and product testing and a dedicated team. Company has 10 manufacturing facilities across seven locations in India.

ISSUE DETAILS

- Issue Open : 17th January, 2018

- Issue Closes : 19th January, 2018

- Issue Type : Book Built Issue IPO

- Face Value : Rs10/ Equity Shares

- Issue Price : Rs.855– Rs.859/ Equity Share

- Valuation : Rs 600 Cr.(Approx.)

- Market Lot : 17 Shares

- Minimum Order Quantity: 17 Shares and in multiples

- Listing At : BSE, NSE

TENTATIVE DATES

- Basis of Allotment(Finalization) : TBU

- Refund Initiation : TBU

- Crediting of Shares : TBU

- Commencement of Trading : TBU

*TBU: To Be Updated

ISSUE OBJECTS

-

(OFS) The offer from the proceeds shall directly go to the selling shareholders. Company will not receive any proceeds from the Offer for Sale by the Selling Shareholders.; and

-

(FRESH ISSUE) The objects for which the Net Proceeds of the Fresh Issue will be utilized are as:

1) Prepayment or repayment of all or a portion of certain borrowings availed by the Company; and

2) General corporate purposes

COMPANY PROMOTERS

Mr. Jasbir Singh , and Mr. Daljit Singh

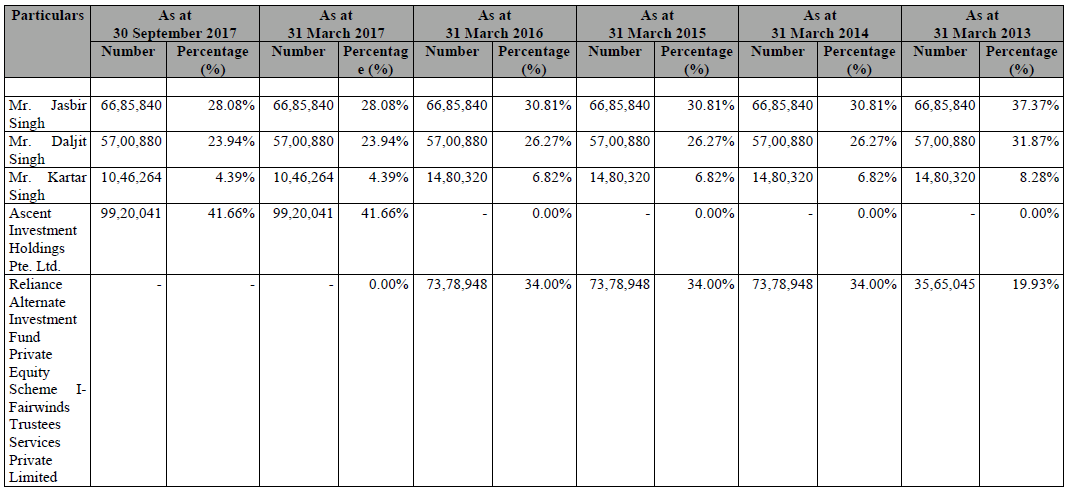

SHAREHOLDERS HOLDING MORE THAN 5% OF SHARES

COMPETITIVE STRENGTHS OF COMPANY

-

Market leadership in the RAC OEM/ODM industry in India

-

One stop solutions provider for the RAC industry with high degree of backward integration

-

Strong customer relationships with the majority of leading RAC brands in India

-

R&D and product design capabilities leading to high proportion of ODM business

-

Track record of financial performance

-

Economies of Scale

-

Culture of innovation and highly experienced management

INDUSTRY OVERVIEW

The Indian RAC market has been witnessing robust growth trend in the past five years with a CAGR of 9.4% by volumes. In the next five years, the market is expected to witness a CAGR of 12.8% reinforced by the surge in rural consumption, shorter replacement cycles, energy-efficient RACs and availability of multiple brands at various price points. The RAC volumes are expected to increase from 4.7 million units in Fiscal 2017 to reach 8.6 million units by Fiscal 2022.

Market Size and Forecast of RAC (Volume in million Units)

RAC Market Penetration – Select Asian Countries and Global

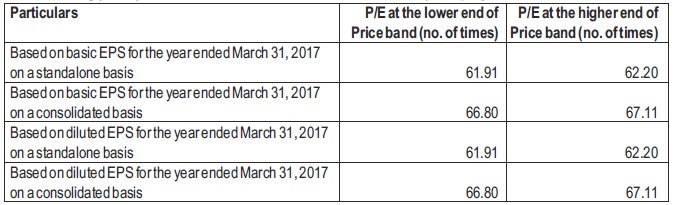

VALUATIONS

As far as Valuations are concerned its hard to determine under valuation of over valuation of the IPO as the company doesn’t have any listed peers but individually it seems to be over-valued with a P/E of 67.11x at the upper price band and 66.80x on lower price band on consolidated basis, on upper price band on standalone basis P/E stands at 62.20x while on lower price band it’s 61.91x.

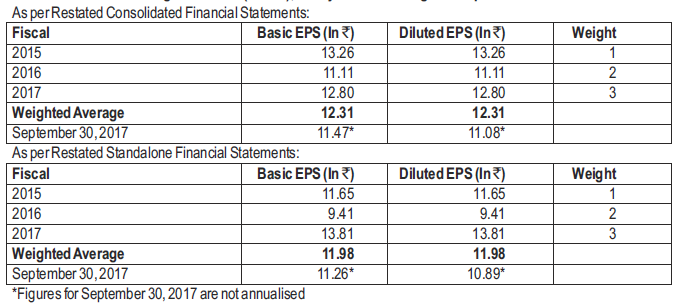

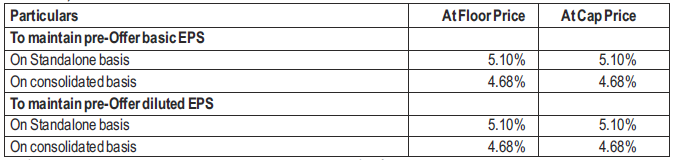

EARNINGS PER SHARE

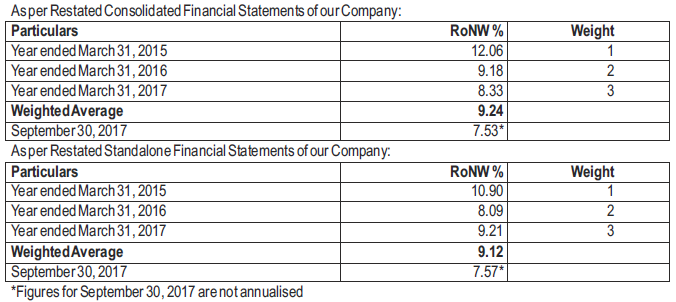

RoNW

Minimum Return on Increased Net Worth after the Offer needed to maintain Pre-Offer EPS for the year ended March 31, 2017

NAV (NET ASSET VALUE)

(i) Net asset value per Equity Share as on March 31, 2017 on a restated consolidated basis is 140.67 and as on September 30, 2017 on a restated consolidated basis is 152.30

(ii) Net asset value per Equity Share as on March 31, 2017 on a restated standalone basis is ` 137.25 and as on September 30, 2017 on a restated standalone basis is ` 148.67

(iii) After the Offer on a restated consolidated basis:

(a) At the Floor Price: ` 273.23

(b) At the Cap Price: ` 273.46

(iv) After the Offer on an restated standalone basis:

(a) At the Floor Price: ` 270.65

(b) At the Cap Price: ` 270.87

COMPARISON WITH LISTED PEERS

The Company does not have any listed industry peers in India.

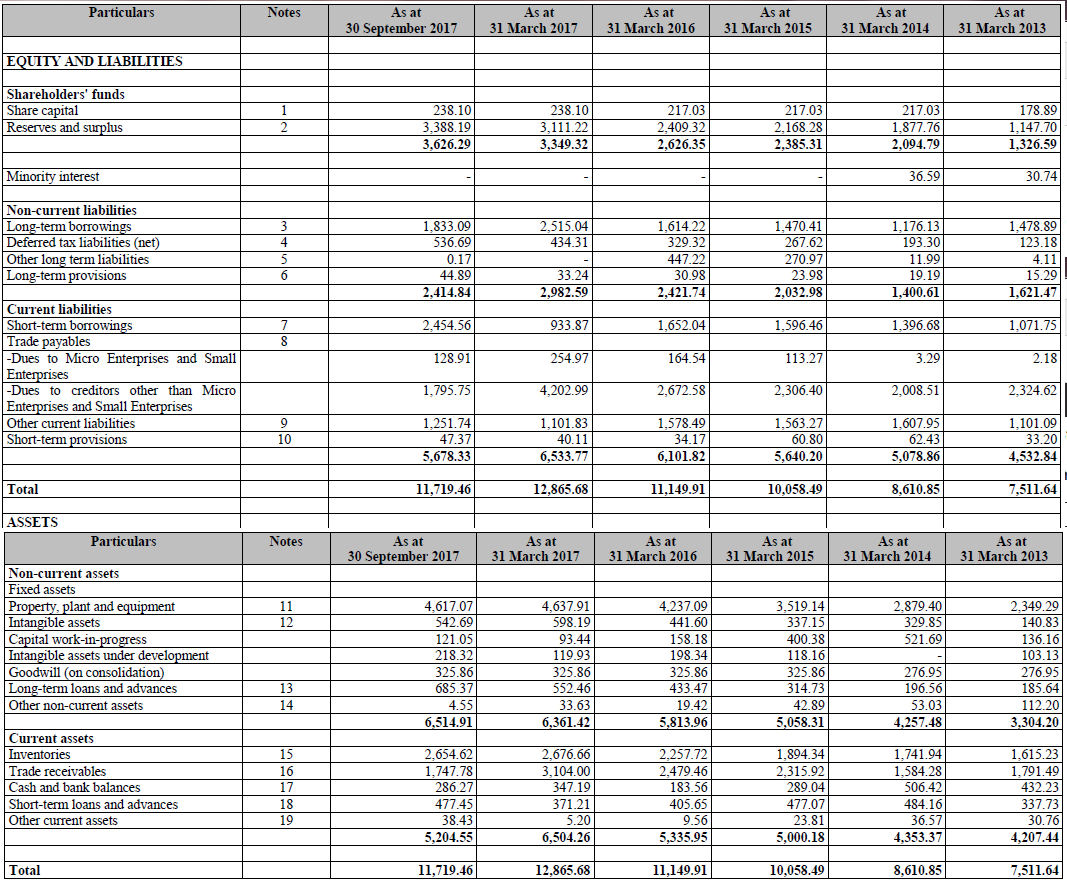

RESTATED CONSOLIDATED FINANCIAL POSITION SUMMARY

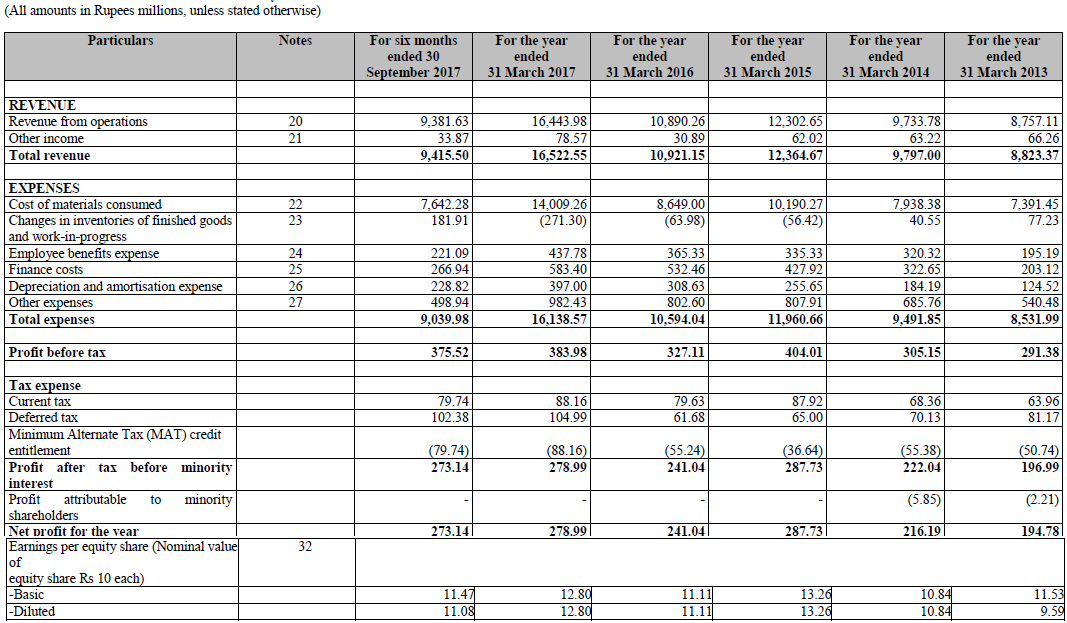

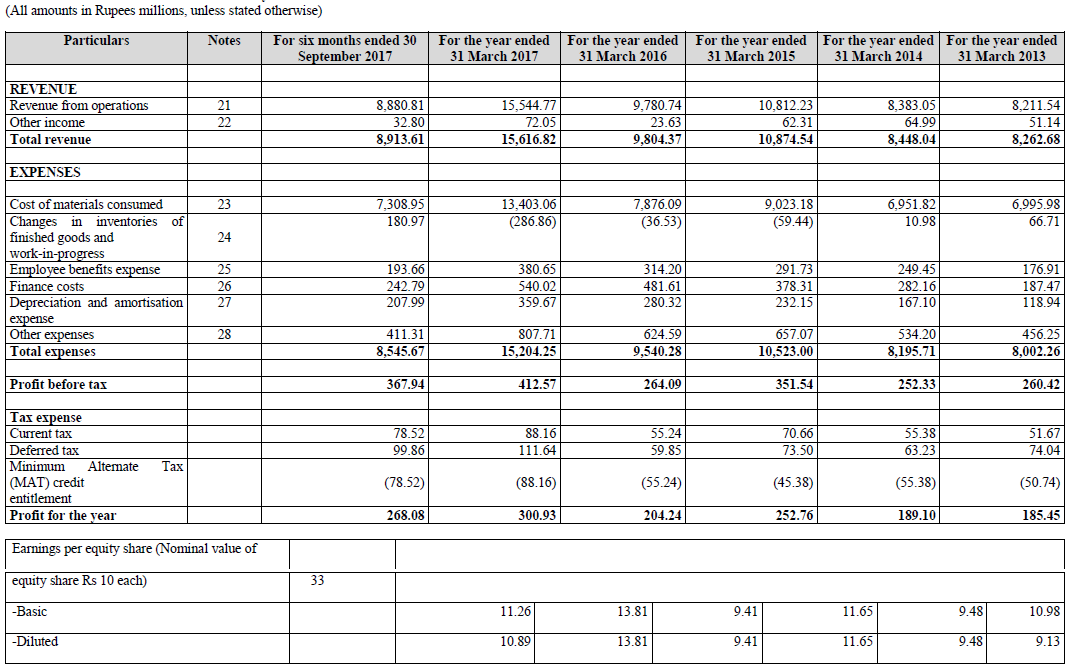

RESTATED CONSOLIDATED STATEMENT OF PROFIT & LOSS ACCOUNT

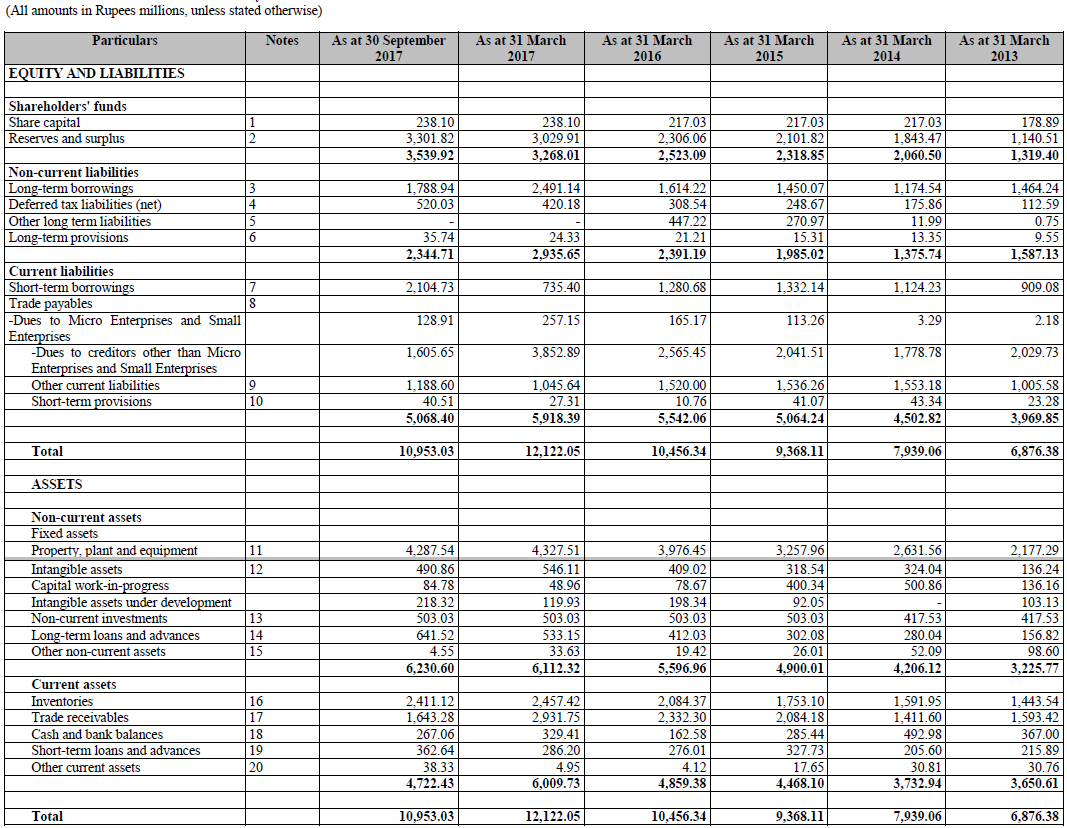

RESTATED STANDALONE FINANCIAL POSITION SUMMARY

RESTATED STANDALONE STATEMENT OF PROFIT & LOSS ACCOUNT

ANALYSIS & SUBSCRIPTION SUGGESTIONS BY AUTHOR

Fellas what makes this fancy is that the company with the market share of 55.4%, Amber is the market leader in the Room Air Conditioner (RAC) design and manufacturing. Amber manufacture these RAC’s for 8 out of the 10 top RAC brands in India including Daikin, Hitachi, LG, Panasonic, Voltas and Whirlpool. These 8 brands have over 75% of market share in India.

Also the company doesn’t seem to have any listed peers. But these factors shall not be the only factors for coming to conclusion. Let’s have a look on major things to consider before rushing to put money in the company:

-

Valuations: As far as Valuations are concerned we do not have any listed peers to have a comparison but individually the issue seems to be over-valued with a P/E @67.10x at upper price band and 66.80x at lower price band. Although we may not have any listed peers but we have a company with almost similar line of business which has a P/E of 67 so comparing to this it seems fairly Valued but this shall not be treated as good measure to consider ,

-

RoNW/EPS: The sharp fall in last three consecutive years in RoNW although in FY2016-17 EPS has shown improvement but that’s not too satisfactory due to RoNW.

-

CAGR: The total revenue has grown at 19.03% CAGR over FY14-17, in comparison with the average revenue of the consumer durable industry, which grew at a CAGR of 11.7% over the said period which seems fancy.

-

Earnings: Earnings except in the FY 2015-16 overall seems consistently in incremental order.

-

Debts: Long term debts have increased over the period that shall also be not ignored which has increased the finance cost of the company.

-

GMP: Trending these days issue’s Grey market premium as on 16th Jan,2018 was at Rs.100-115

Fellas lot of things already mentioned above have shown mixed view towards the issue infact GMP makes us eager for the subscription and the company seems to have monopoly(As no listed peers) but we may not forget the issue seems to be over-valued and RoNW too is not satisfactory but the company has good market capture so one may consider for subscribing the issue for medium to long term perspective only however if anyone still wants to subscribe the issue for listing benefits as well then one should wait and see if the issue gets over-subscribed by minimum 20 times of more then one shall consider for some good listing gains.*

*Disclaimer: Author may or may not have interest in the issue, before getting to conclusion consult your Financial Adviser. The Author shall not be responsible for any kind of loss of gain arising out of any investments. All data were taken from RHP filled to SEBI by the company.